|

|

| Help | |

| You are here: Rediff Home » India » Business » Special » Features |

|

| |||||||||||||||||||||||

|

| |||||||||||||||||||||||

The Securities Contracts (Regulation) Amendment Bill, 2007, recently passed by Parliament, might make a bigger difference to your life than you thought. In the medium to long term, its success or failure could partly determine what interest rate you pay on your home loans.

The concept

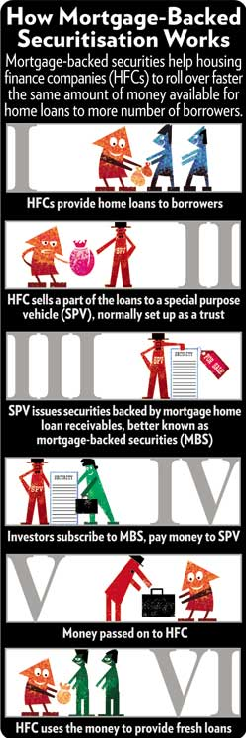

When a bank or a housing finance company gives loans, the borrowers' assets stay in its books till the loan matures. Securitisation helps the bank monetise some of these assets and advance further loans. (See graphic: How Mortgage-Backed Securitisation Works)

The US story

Securitisation, in its present form, originated in the mortgage markets of the US. The US government encouraged secondary markets in mortgages, starting from February 1970.

Reports say the volume of agency mortgage-backed securities in the US went up from $110.9 billion in 1980 to $2,634.9 billion on June 2001. Government sponsored securitisation agencies like Ginnie Mae, Fannie Mae and Freddie Mac try to make low-cost finance available to Americans.

Vinod Kothari, securitisation expert and executive director of Asian Securitisation Forum, says, "In the last 30 years, the spread (difference in the prime lending rate and the treasury rates), in the US has come down, making loans more affordable."

The Indian situation

According to ICRA's Update on Indian Structured Finance Market (July 2005), the volume of mortgage-backed securities in India has increased from Rs 80 crore (Rs 800 million) in FY02 to Rs 5,010 crore (Rs 50.10 billion) in FY06. The report also says: ". . .the MBS market has a potential for higher growth. However, the long tenure of the MBS paper, together with the lack of secondary market liquidity deters certain investors from investing in it."

As Prasad Koparkar, head (structured finance ratings), Crisil, explains, "Prior to this Bill, a securitised paper could not be traded on stock exchanges." While a limited number of bilateral deals continue to take place, liquidity for such papers is very limited.

This impacts the attractiveness of the paper for many investors. The problem is exacerbated for long-term securitised papers like MBS (since home loan tenures are now typically 20 years or more, MBS backed by these loans also have corresponding longer maturities)."

The Bill is set to resolve the issue of liquidity. If it does, you might see your home loan rates going down again.

The impact of the amendment

Experts are unanimous that though the impact of the Bill will not reduce the cost of loans immediately, but in the long run they are likely to make loans more affordable.

Says Koparkar, "With the amendment, listing will be possible for securitised paper. This can improve the liquidity of such papers. A broader and deeper market can, over a period of time, lower the yield on such papers." This, in turn, would reduce the funding cost for HFCs, which can translate into lower home lending rates, he says.

Kothari agrees, "This will lead to the integration of the mortgage market and the capital market. Securitisation reduces the asset liability mismatch in a bank's balance." We can even expect the prime lending rates to come down in India too, he adds.

The caveats

However, Koparkar warns that though the Bill has addressed the issue of liquidity, issues like stamp duty and investment guidelines for long-term investors like insurance companies and pension funds need to be modified to derive full benefit of such innovative structures and help lending rates come down. The lack of availability of credit information of consumers can also play spoilsport.

More Specials

Powered by

|

|

| © 2007 Rediff.com India Limited. All Rights Reserved. Disclaimer | Feedback |