Recovery of the Indian economy depends to a great extent on acceleration in the spending of these relatively richer households, explains Mahesh Vyas.

Thanks to the second wave of COVID-19, India's economic recovery process is stalled.

What will spur growth again? The recovery cannot be investments-led because most enterprises are nursing excess capacities.

It is also evident that the government is reluctant to spend its way out of the economic crunch.

Can households bail out the Indian economy? Prima facie, it seems difficult because households have seen a fall in income and their expectation of a return to better times is very low.

In April 2021, only 4.2 per cent of households said that their incomes were higher than a year ago and only 5.2 per cent said that they expect their incomes to go up in a year.

These proportions used to be 33 per cent and 30 per cent in 2019-20. It's a very long journey to get back to normal times.

What matters from the point of view of calculating the recovery is the status of the relatively well-off households.

If we are seeing a K-shaped recovery then, can the upper-arm of the K pull the country out of its current morass? This is the question that Latha Venkatesh asked me recently.

It is a question that merits a better answer than what I gave her on the CNBC-TV18 show she was hosting.

It is an important question because it is the upper arm of the K that drives consumption from the organised sectors. And, in the short term, it is the organised sector that drives GDP growth calculations.

Therefore, growth in the consumption of the relatively well-off households makes a big difference to India's economic recovery story -- at least the one captured by the GDP data.

The popular perception is that while many of the salaried employees have lost jobs, generally, households of the relatively affluent salaried employees presumably continued receiving income flows but the various forms of lockdown curtailed their spending.

Thus, this class was forced to save. These savings found their way into the equity markets which in turn have obliged with superfluous returns.

The richer could have got wealthier by appreciation in valuation of their investments if not by wages.

Recovery of the Indian economy depends to a great extent on acceleration in the spending of these relatively richer households. What does this class tell us about its well-being and its outlook?

First, let's define this class. The average household income in 2019-2020, according to CMIE's Consumer Pyramids Household Survey was Rs 245,000.

To understand the condition of the relatively affluent households we study those that have an annual income that is more than twice or more than four times this average -- those that have an annual income of Rs 500,000 to Rs 1,000,000 and those who earn more than a million rupees a year.

Prima facie evidence suggests that as of the quarter ended December 2020 incomes at the upper end of the income pyramid were much smaller than levels a year ago.

Income of households with annual income of a million or more rupees was 14.5 per cent lower than in the December 2019 quarter.

Households with income of less than a million rupees saw their incomes shrink by less than one per cent in a similar comparison.

Apparently, even a small hit in income can hurt consumer sentiments disproportionately.

Consumer sentiments are much worse than what the fall in incomes tell us.

The Index of Consumer Sentiments of households that earn more than a million rupees in the quarter ended December 2020 was 48 per cent lower than it was in the quarter ended December 2019.

Consumer sentiments of households that earned less than a million were down by over 50 per cent in the same comparison.

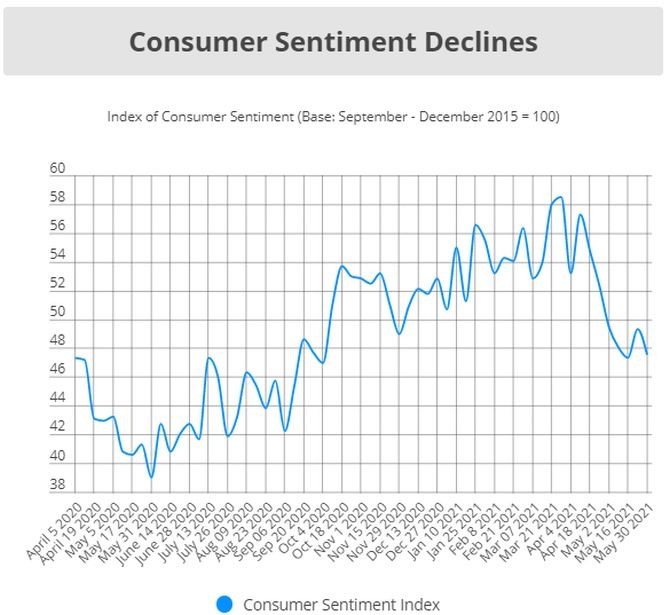

Consumer sentiments data is more up-to-date than income data that is available only till December 2020.

These show an improvement in the quarter ended March 2021. But, sentiments declined again in April, the month when the second wave of Covid-19 peaked in India.

In April 2021, 11.8 per cent of the richer households, those that earned more than a million rupees a year, said that their incomes were higher than they were a year ago.

A rather large, 36 per cent said that their incomes were worse than they were a year ago.

The biggest spoiler to the expectation that the top arm of the K in the K-shaped recovery would power India out of the abyss is its sudden elevated pessimism.

In April 2021, less than six per cent of the richer households said that they expected their incomes to be better in a year.

This is half of the proportion who claimed to have seen an improvement in their incomes compared to a year ago.

This is also half of the respondents who believed in the preceding four months, that their incomes would improve in the coming year. Sentiments have suddenly worsened for the richer people in April.

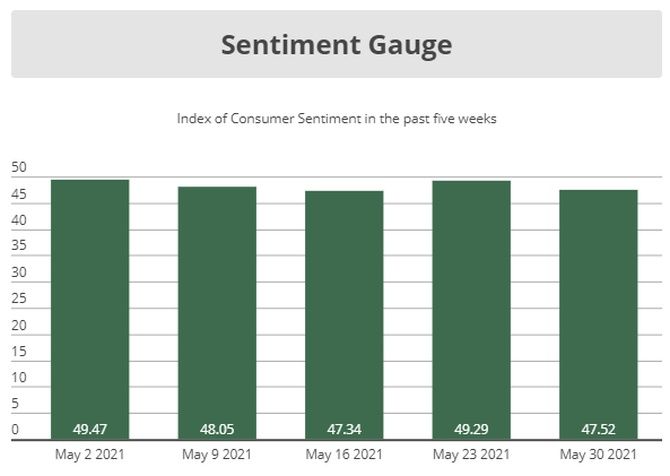

We know that sentiments worsened further during May 2021.

The Index of Consumer Sentiments was at 54.4 (base: 100 in September-December 2015) in April 2021. It was at 48.6 as of May 30, 2021.

It is unlikely that the richer households have fared better. India needs household incomes and their sentiments to improve substantially before it can hope that they would contribute to the recovery process.

Currently, households need help.

Mahesh Vyas is MD and CEO, CMIE P Ltd.

Feature Presentation: Rajesh Alva/Rediff.com

© 2025

© 2025