The rupee weakened on Monday, snapping two days of gains after data showed higher-than-expected inflation for September and robust dollar demand from a large private oil firm.

The rupee weakened on Monday, snapping two days of gains after data showed higher-than-expected inflation for September and robust dollar demand from a large private oil firm.

Traders are also awaiting the outcome of talks to raise the US debt limit to avoid what would be a historic default.

The dollar slipped and the yen gained on safe-haven demand.

"It was largely a very dull market domestically," said Uday Bhatt, a foreign exchange dealer with UCO Bank.

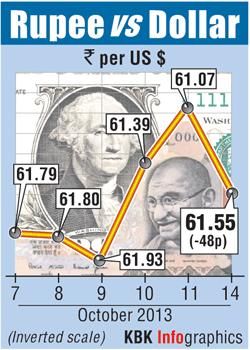

"All eyes are on the US for now. We could see the pair holding in a 60.80 to 62.50 range until there is clarity from the US." The partially convertible rupee closed at the day's low of 61.55/56 per dollar compared with 61.07/08 on Friday, after moving in a 61.13 to 61.55 range.

India's wholesale price index rose 6.46 percent in September from a year earlier, well above expectations of a 6.0 percent advance and above the 6.1

The data is making more likely the Reserve Bank of India will raise interest rates by 25 basis points on October 29, which would mark the second consecutive monthly hike.

India is due to report consumer price inflation data around 1730 local time (1130 GMT).

Several traders also cited dollar demand from a large private oil firm in late trade which led to a spike in the USD/INR pair.

The demand was worth around $100 million, said a trader, adding it was not a large amount but enough to move markets given the lower trading volume.

In the offshore non-deliverable forwards, the one-month contract was at 62.08, while the three-month was at 63.03.

In the currency futures market, the most-traded near-month dollar/rupee contracts on the National Stock Exchange, the MCX-SX and the United Stock Exchange all closed at around 61.71 with a total traded volume of $1.70 billion.

© 2025

© 2025