Backed by good numbers posted by frontline software services players, there has been an uptick in the March quarter revenues and profits of the 129 firms that have declared their financial results so far.

Backed by good numbers posted by frontline software services players, there has been an uptick in the March quarter revenues and profits of the 129 firms that have declared their financial results so far.

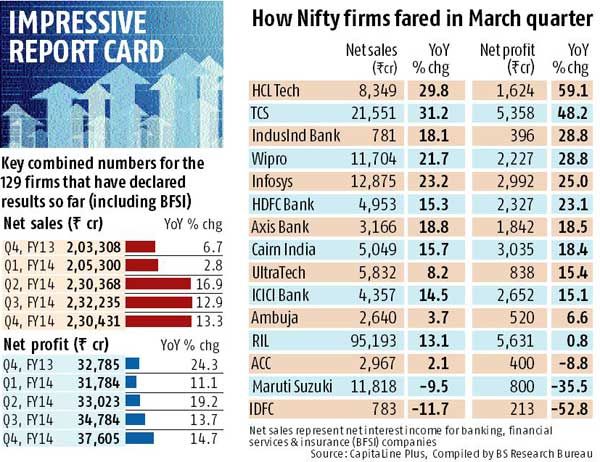

This universe of (129) companies has seen its revenue growth improving 13.3 per cent on a year-on-year basis, compared with 12.9 per cent in the previous quarter.

On an annual basis, net profit growth, too, has been better at 14.7 per cent, compared with 13.7 per cent in the December quarter.

Better sales and profit growth rates in 2013-14 were seen only in the September quarter (see chart).

Even if banking & financial services companies were to be excluded, the revenue and profit growth trend would be little changed.

The strong overall numbers have much to do with an impressive show by the information technology sector, especially the big four companies, which saw their earnings grow 39 per cent and revenue 27 per cent, on a year-on-year basis.

Analysts believe strong deal pipelines, better efficiencies and improving utilisation rates helped improve the IT majors’ performance.

Private banks and financial services firms, too, had a reasonable quarter, given an apparent slowdown in the economy.

The net interest income (the difference between interest income and interest expense) for top private banks was up 16 per cent, while earnings growth was higher at 19 per cent.

Also, asset quality was stable, with private banks’ managements expecting to clock higher loan growth than the industry average.

“It is still early to draw a conclusion, but I think private banks have done well and most have exceeded expectations.

“This shows banks have managed the economic downturn very well,” says Rajat Rajgarhia, managing director (institutional equities), Motilal Oswal Securities.

Given the results of the top companies so far, analysts say the Sensex/Nifty companies are on course to achieve 12 per cent year-on-year earnings growth for the March quarter.

The 15 Nifty companies that have declared their results so far have posted year-on-year net profit growth of 17 per cent and a combined revenue growth of 14.5 per cent.

Most companies have been able to manage their costs well, leading to an improvement in their operating profit margins.

Most companies have been able to manage their costs well, leading to an improvement in their operating profit margins.

Both for the broader universe of stocks and the Sensex/Nifty companies (including banks and financial services), profit margins for the March quarter have been the highest in 2013-14.

Margins were aided by benign input costs and other expenses, which grew 9.5

Among IT majors, Infosys, Wipro and HCL Tech saw their margins expanding due to a decline in selling, general and administrative expenses, higher utilisation and (in the case of Wipro) higher proportion of fixed price contracts.

Top cement companies (except ACC), too, reported higher profits, slightly ahead of estimates.

Ambuja was able to keep a lid on costs, while UltraTech Cement reported a 15 per cent year-on-year increase in profits, despite rise in costs.

The profit beat for UltraTech was largely due to tax reversal. Nevertheless, excluding that, it was marginally ahead of estimates.

V Srinivasan, who tracks the sector at Angel Broking, says: “While most cement companies have reported better-than-expected net profits, realisations will be something to watch out for, since these were disappointing.

“Companies have been able to control costs. That, to some extent, helped the companies report higher profits.”

In addition to realisations, analysts have also highlighted issues pertaining to volume growth, as demand continues to be sluggish.

A lack of demand was also reflected in the numbers posted by Maruti Suzuki, which saw its sales falling nine per cent annually on lower volumes; and margins 213 basis points due to dealer compensation (on old inventory) and higher raw material and employee costs.

Analysts, however, say new model launches and demand recovery should help India’s largest carmaker post better numbers going ahead. Maruti isn’t alone.

Among the few companies that have not done well are IDFC, which has seen profits nosedive on higher provisioning for stressed assets.

Analysts believe, given the performance in a tough economic environment, a recovery could see many domestic companies grow at a faster pace.

KR Choksey’s Deven Choksey says: “Domestic companies that have been resilient in the slowdown could bounce back strongly when higher economic growth returns.”

While Reliance Industries Ltd’s numbers have been marginally lower than expected, the silver lining is a jump in operating profits and better refining margins.

So far, there has not been any impact on account of interest costs, as early birds like IT firms, cement majors, RIL and Maruti are sitting on cash or have negligible net debt on their books.

The interest costs could come into play later, given that some of the leveraged plays in the infrastructure sector will release their results.

Experts say, while the rupee is still 14 per cent lower vis-à-vis the dollar on a year-on-year basis, so far, there has not been any impact of the currency’s sequential fall on results.

That’s because the change in the currency’s value, according to analysts, has been gradual and steady.

© 2025

© 2025