T

The Street is unimpressed by the results of the top three pharma companies, but given the share price correction and earnings outlook, there are gains to be made.

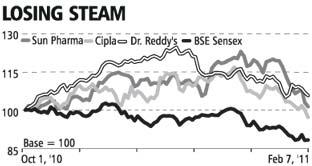

India's largest pharma companies by market capitalisation Sun Pharma, Dr Reddy's and Cipla have seen their share prices drop 5-20 per cent over the last two weeks on results that were below Street expectations.

Cipla and Sun Pharma as well as the BSE Healthcare index have been underperforming the broader markets, which have fallen 5.8 per cent over the same period.

Lower than expected net profits have prompted analysts to revise downwards their earnings estimates for the three companies.

Cipla is expected to report nearly 10 per cent growth in earnings in 2011-12. There is a limited upside for its stock from the current levels, given the analysts' price target of Rs 338.

In contrast, Sun and Dr Reddy's are expected to post a robust 26-28 per cent earnings growth in the next financial year.

And given the recent correction in their share prices and analysts' price targets of Rs 469 and Rs 1,744, respectively, there is a decent upside from the current levels.

| MARGIN PRESSURES |

| In Rs cr |

Cipla |

Dr Reddy's |

Sun Pharma |

| Sales |

1,568 |

1,899 |

1,601 |

| % change y-o-y |

8.0 |

10.0 |

56.0 |

| Ebitda margins (%) |

20.3 |

21.0 |

27.5 |

| Change (bps) |

-590 |

0 |

-280 |

| Net profit |

232 |

273 |

350 |

| % change y-o-y |

-19.5 |

LTP* |

3.5 |

| P/E FY11E (x) |

22.4 |

26.4 |

24.4 |

| P/E FY12E (x) |

20.2 |

20.8 |

18.9 |

Financial figures are on consolidated basis and for quarter ended December 2010

Sun's numbers include those of Taro Pharma

*Loss to Profit E: Estimates Source: Companies, Analyst reports |

Sun Pharma A large part of the growth in Sun Pharma's consolidated revenues came from its Israel-based subsidiary acquired in the September 2010 quarter, which contributed 28

per cent to the quarter's sales.

Ex-Taro sales grew just 12 per cent, which were in line with expectations though.

Consolidated net profits grew just 3.3 per cent on account of higher staff costs and depreciation charges on account of Taro.

Going ahead, on account of the Taro consolidation, Sun has guided for a 42 per cent sales growth for 2010-11 as against 35 per cent earlier.

Sharekhan analysts believe this is conservative, considering the company has grown 51 per cent in the fiscal so far and has projected a growth of 31 per cent in the March quarter.

Consolidated Ebitda margins (28 per cent in the quarter) are likely to decline for the full year (2010-11) as Taro earns margins of around 20 per cent compared with Sun Pharma's 34-35 per cent. Sun's domestic formulations business recorded a 22 per cent jump on the back of nine new launches and is expected to maintain its strong performance.

However, growth in its US subsidiary, Caraco, would be in the region of 9-11 per cent over FY11-13, with no one-off revenues in the March quarter, says a Sharekhan report.

Clarity on the financials of Taro will emerge once the audited reports for CY2009 are published.

Dr Reddy's Laboratories Contribution from new products launched in the US helped the company post a 10 per cent year-on-year consolidated sales growth for the December quarter.

Analysts at RBS Equities say these numbers are below expectations as excluding revenue contribution from new products, revenues were flat with core US operations growing just 5 per cent.

Net profits were also below estimates, believe Enam analysts, because of higher litigation costs in the US, refinancing costs of debt at its German subsidiary Betapharm and marketing costs in India and Russia.

The management expects the US revenues to be strong in the March quarter on the back of new launches and the contribution from recently launched products.

It expects Betapharm to face pricing pressures due to its tender business model. Revenues from India were up 14.5 per cent year-on-year to Rs 301 crore (Rs 3.01 billion) on the back of volume growth as well as the launch of products over the last one year.

The company is expecting strong growth in the domestic segment in the coming quarters on the back of new launches and strengthening of its field force.

Cipla Cipla reported unimpressive figures for the December quarter on a lower than expected domestic sector performance due to increasing competition.

Operating profit margins, which were hit by the costs associated with the setting up of the Indore plant, appreciation of the rupee and lower technology know-how and fees, are likely to come under pressure.

The fall in net profits was on account of lower operating profit margins and a 42 per cent jump in depreciation on account of the Indore plant.

The operational costs related to the Indore plant (about Rs 30 crore a quarter) are likely to impinge on margins in the near term, till the output scales up.

The company, in its post-results conference call, indicated it may file its own ANDAs (abbreviated new drug delivery applications) in the US market.

Citigroup analysts Prashant Nair and Anshuman Gupta believe while this is a long-term positive, it could hurt profitability in the near term.

The Street is unimpressed by the results of the top three pharma companies, but given the share price correction and earnings outlook, there are gains to be made.

The Street is unimpressed by the results of the top three pharma companies, but given the share price correction and earnings outlook, there are gains to be made.