'The slowdown in motor insurance premium growth is due to slower growth in vehicle sales. Also, there has been minimal hike in third-party rates in the past three years which is affecting the growth rate of third-party premiums.'

Sluggish domestic vehicle sales, stagnant third-party insurance rates, and stiff competition are slowing down growth in motor vehicle insurance premiums.

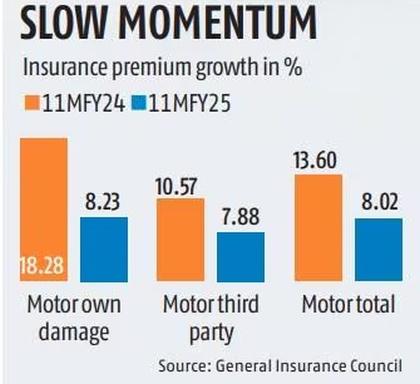

Premium growth has slowed from 13.6 per cent in the April-February period of 2023-24 (FY24) to 8 per cent in the same period of 2024-25 (FY25).

Overall motor vehicle insurance premiums stood at ₹89,405 crore in the April-February period of FY25.

Within the segment, growth in third-party premiums is down from 10.57 per cent last year to 7.88 per cent this year.

Growth in 'motor own damage' premiums has dropped from 18.28 per cent last year to 8.23 per cent this year.

“The motor insurance segment in India is witnessing slow premium growth this financial year mainly due to very high competition among insurers,” said Shashi Kant Dahuja, executive director and chief underwriting officer, Shriram General Insurance.

Dahuja explained that to get more market share, some insurers have started offering heavy discounts, which is negatively affecting overall premium growth in the industry.

“Many insurers adopt a “lowest price” (L1) strategy to stay competitive, further driving down premium rates.”

“Passenger vehicle domestic sales have remained tepid, which has resulted in lukewarm 'motor own damage' growth. In the meantime, flat motor third-party rates continue to slow the growth of motor third-party (premiums),” analysts at ratings company CareEdge said in a report.

According to data from the Federation of Automobile Dealers Associations, retail vehicle sales grew 7.05 per cent in the April-February period of FY25.

In February 2025, retail vehicle sales declined 7.19 per cent year-on-year.

“The slowdown in motor insurance premium growth is due to slower growth in vehicle sales. Also, there has been minimal hike in third-party rates in the past three years which is affecting the growth rate of third-party premiums,” said Neha Parikh, vice president and sector head – financial sector ratings, ICRA.

The current motor third-party rates came into effect on June 1, 2022 and have not been revised since.

“Growth in the motor segment remains contingent on momentum in vehicle sales and changes in third-party tariffs,” analysts at CareEdge said.

Feature Presentation: Rajesh Alva/Rediff.com

© 2025

© 2025