''We continue to believe that the global economy will narrowly avoid a recession, despite expecting the US, Canada, and most of Europe to fall into recession at some point over the next year or so.'

Inflation is on an upward trend in almost all the countries around the world.

With the interest rate hikes in the US, many central banks around the world are tightening their monetary policy.

The European Central Bank has increased its policy rate followed by the Bank of England and the Bank of Canada.

Other countries following suit are Australia, India and many countries in Latin America.

The R word is now spoken not in whispers. Some reports say the world is already in recession. Others say, 2023 will be a tough year for the world.

"We may fall into recession, but it will be mild compared to the past recession periods," Ben May, director of global macroeconomic research at Oxford Economics, left, bottom, who is involved in the production and presentation of the company's global macroeconomic views, tells Rediff.com's Shobha Warrier.

We have had two recessions in the 1980s, then the 1997 Asian crisis, the dotcom bust, the 2008 global financial crisis and the latest crisis due to the pandemic.

How different is today's global financial situation compared to the earlier crises?

First, the global economy is not in recession yet. It is weak, but not quite into recession territory.

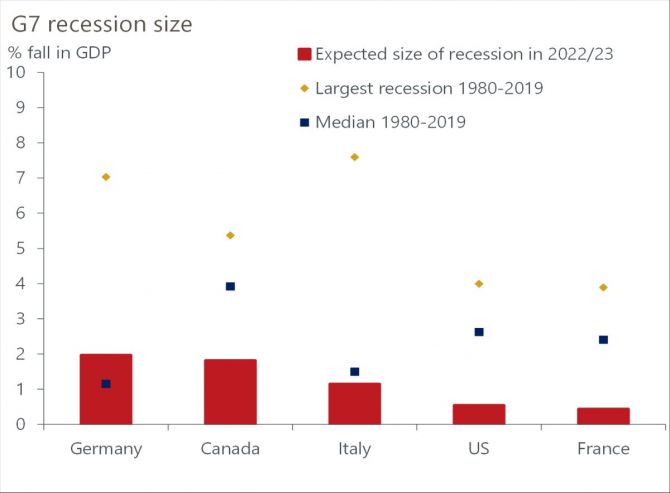

We may fall into recession, but it will be mild compared to the past recession periods.

We continue to believe that the global economy will narrowly avoid a recession, despite expecting the US, Canada, and most of Europe to fall into recession at some point over the next year or so.

Avoidance of a global contraction while several large economies fall into recession wouldn't necessarily be an unusual outcome.

It's worth noting that all the five US technical recessions since 1980 have coincided with a global recession.

But we expect the upcoming peak to trough GDP fall in the US to be far smaller than in any of the previous five slumps.

Therefore, it is reasonable to believe a global recession could be avoided.

Your report says the fall will not be of long duration but it will last only 2 or 3 quarters in 2023. What signal are you getting that tells you it will be of shorter duration?

Since the 1980s, there have been nine advanced economy recession clusters, but only five of these have coincided with two or more consecutive quarterly falls in global per capita GDP -- the benchmark for a global recession.

The first thing is, a lot of downward slide we are seeing so far has been due to the enormous shocks such as the high gas prices due to the Russia-Ukraine war, the supply chain issues due to lockdowns, high inflation and more recently the policy timing in the US.

We also see that most of these issues will dissipate next year. As we move into the second half of the year, economic growth could begin to pick back up.

The low point will be perhaps early next year, and after that, things will start getting better.

The Oxford Economics risk perception survey says, businesses see a 50% chance of a global recession in the next 12 months.

We talk a lot about the economy going into a recession or not. But in many sense, recession is an arbitrary threshold.

The difference of narrowly avoiding recession or just falling into recession is likely to be fairly small in the grand scheme of things.

Regardless of whether the global economy falls into recession, we are going to see very weak growth across economies, even by the standards of global financial crisis period.

Our benchmark for recession is negative per capita GDP growth for two consecutive quarters.

We continue to believe the global economy will narrowly avoid a recession, despite expecting the US, Canada, and most of Europe to fall into recession at some point over the next year or so.

You said, while the US, Canada and the whole of Europe might feel the recession, the Asia Pacific region will not. Why do you say so?

The positives for Asia is, China in the course of the next six months, may stage a strong comeback after the lockdown, which will help its neighbours.

Inflation is less of a concern in parts of Asia. And there is perhaps more easy growth win from a return to normalcy in some Asian economies, particularly with respect to tourism.

Because of the continuous lockdown due to China's zero covid policy, the entire world is facing supply chain issues.

Do you see manufacturing shifting to other parts of the world now, with a lot less dependency on China?

What we have been seeing in the recent years is, some instances of manufacturing going away from China.

A lot of that is because of China becoming more expensive.

It is a natural development, not deglobalisation.

Unlike the dotcom bust which affected mainly one sector and the financial crisis, do you think this crisis will affect the entire globe and across all spectrum?

I think, the nature of some of these shocks causing slow growth is going to be global in nature hitting some places harder than the others.

Some economies will suffer more than the others which we saw in the earlier crises too.

For example, we expect the Asian economies to get less affected this time than North America, the whole of Europe or Canada.

The gas prices in Europe is a very major factor, a very specific shock affecting that region, and the policy timing in the US.

The silver lining according to your report is this recession will be of shorter duration...

That's our feeling at the moment. By historical comparisons, recessions in the advanced economies are expected to be small and short.

That's the positive. If some more shocks come along, then things could get worse.

We don't see a very nasty recession like the financial crisis or the pandemic.

Feature Presentation: Aslam Hunani/Rediff.com

© 2025

© 2025