'The telecom companies are our lifeline now, despite having nearly collapsed under debt because of ill-advised policies.'

'Perhaps our obvious dependence on telecom services will spark well-conceived policies for this sector,' says Shyam Ponappa.

This is a time when, as the authorities deal with a lockdown, there needs to be an equal emphasis on providing for large number of people without the money for food and necessities, while the rest of us wait it out.

Hard as it is, an MIT scholar writes that after the Spanish flu in 1918, cities that restricted public gatherings sooner and longer had fewer fatalities, and emerged with stronger economic growth.

It is likely that costs and benefits vary with economic and social capacity, and we may have a harder time with it here.

Going forward, government action to help provide relief, rehabilitate people and deal with loss needs to be well planned, including targeting aid to the urban and displaced poor.

As important now as to ensure the lockdown continues is to plan on how to revive productive activity and the economy, and restore public confidence.

A systematic approach will likely yield better results.

A major element of the recovery plan is steps such as liberal credit and amortisation terms, perhaps much more than the three-month extension the Reserve Bank of India has announced.

A primary purpose is the re-initiation of large-scale activities such as construction, of which there are reportedly about 200,000 large projects around the country.

These have to be nursed back to being going concerns.

The RBI may need to consider doing more, including lowering rates.

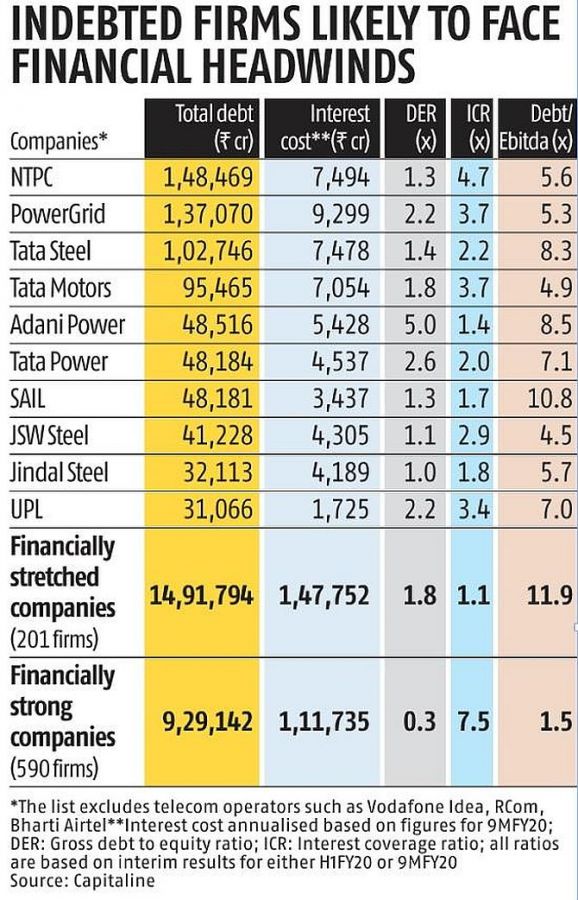

An ominous development that has grown as the economy slowed is financial stress that could swell non-performing assets.

At the half-year ending September 2019, about half of non-financial large corporations in India, excluding telecom, showed financial stress (see table).

These include some of India's largest companies, producing power, steel, and chemicals.

The 201 companies have total debt of nearly Rs 15 trillion, more than half of all borrowings.

There is also the debt overhang of the National Highways Authority of India, and of the telecom companies.

Ironically, the telecom companies are our lifeline now, despite having nearly collapsed under debt because of ill-advised policies in the past which have still not changed.

Perhaps our obvious dependence on telecom services now will spark well-conceived, convergent policies for this sector, so that we can function effectively.

A start with immediate changes in administrative rules for 60GHz, 70-80GHz, and 500-700MHz wireless use, modelled on the US FCC regulations as was done for the 5GHz Wi-Fi in October 2018 could change the game.

It will provide the opportunity in India for the innovation of devices, their production, and use, possibly unleashing this sector.

This can help offset our reliance on imported technology and equipment.

However, such changes in policies and purchasing support have eluded us thus far.

Now, the only way our high-technology manufacturers can thrive is to succeed internationally, in order to be able to sell to the domestic market.

Imagine how hard that might be, and you begin to get an inkling of why we have few domestic product champions, struggling against odds in areas such as optical switches, networking equipment, and wireless devices.

For order-of-magnitude change, however, structural changes need to be worked out in consultation with operators in the organisation of services through shared infrastructure.

For the longer term, a fundamental reconsideration for allocating resources is needed through coherent, orchestrated policy planning and support.

What the government can do as a primary responsibility, besides ensuring law and order and security, is to develop our inadequate and unreliable infrastructure, including facilities and services that enable efficient production clusters, their integrated functioning, and skilling.

For instance, Apple's recent decision against moving iPhone production from China to India was reportedly because similar large facilities (factories of 250,000) are not feasible here, and second, our logistics are inadequate.

Such considerations should be factored into our planning although Apple may well have to revisit the very sustainability of the concept of outsize facilities that require the sort of repressive conditions prevailing in China.

However, we need not aim for building unsustainable mega-factories.

Instead, a more practical approach may be to plan for building agglomerations of smaller, sustainable units, that can aggregate their activity and output effectively and efficiently.

Such developments could form the basis of numerous viable clusters, and where possible, capitalise on existing incipient clusters of activities.

Such infrastructure needs to be extended to the countryside for agriculture and allied activities as well, so that productivity increases with a change from rain-fed, extensive cultivation to intensive practices, with more controlled conditions.

The automotive industry, the largest employer in manufacturing, provides an example for other sectors.

It was a success story like telecom until recently, but is now floundering, partly because of inappropriate policies, despite its systematic efforts at incorporating collaborative planning and working with the government.

It has achieved the remarkable transformation of moving from BS-IV to BS-VI emission regulations in just three years, upgrading by two levels with an investment of Rs 70,000 crore, whereas European companies have taken five to six years to upgrade by one level.

This has meant that there was no time for local sourcing, and therefore heavy reliance on global suppliers, including China.

While the collaborative planning model adopted by industry provides a model for other sectors, the question here is, what now.

In a sense, it was not just the radical change in market demand with the advent of ridesharing and e-vehicles, but also the government’s approach to policies and taxation that aggravated its difficulties.

Going forward, policies that are more congruent in terms of societal goals, including employment that support the development of large manufacturing opportunities, need to be thought through from a perspective of aligning and integrating objectives (in this case, transportation).

Areas such as automotive and other industries for the manufacture of road and rail transport vehicles need to be considered from the perspective of reconfiguring the purpose, flow, and value-added, to achieve both low-cost, accessible mass transport, and vehicles for private use that complement transportation objectives as also employment and welfare.

Systematic and convergent planning and implementation across sectors could help achieve a better revival.

© 2025

© 2025