The recent improvement in consumer sentiment is almost entirely a rural India story.

Much of the corporate sector reposes faith in rural India to fuel its growth, observes Mahesh Vyas.

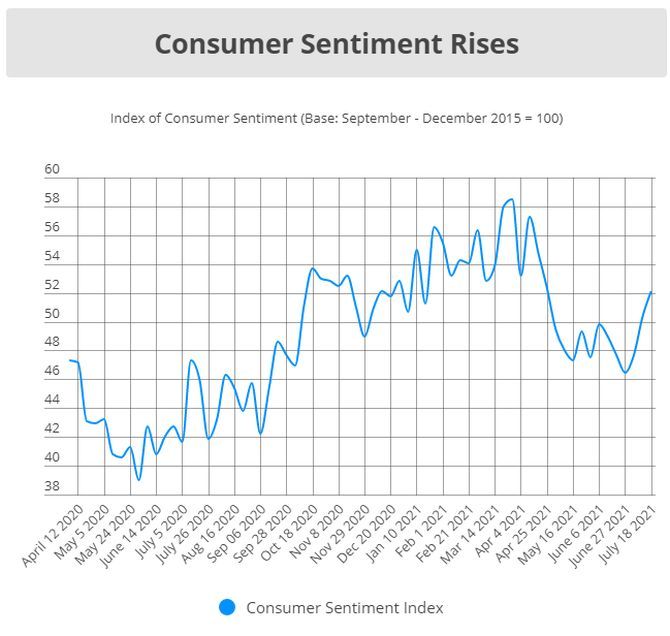

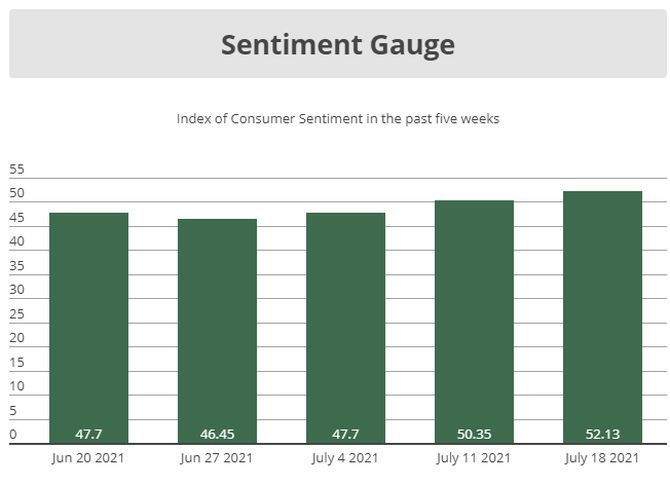

Consumer sentiments seem to be turning around in July. The week ended July 18 was the third in a row when the Index of Consumer Sentiments registered an increase.

Cumulatively, the index climbed 12.2 per cent over these three weeks since June 27.

Consumer sentiments, badgered by the second COVID-19 wave, had been falling steadily from the beginning of April 2021.

It fell more than 20 per cent from its recent peak of 58.5 on March 28 to a low of 46.5 on 27 June.

This fall seems to have bottomed out in late June.

The recent improvement in consumer sentiment is almost entirely a rural India story.

Cumulative consumer sentiments improved by 17 per cent during the past three weeks in rural India.

The improvement here was also steadily robust in each of the three weeks.

The Index of Consumer Sentiments for rural India scaled up by 4.3 per cent in the week ended July 4, then by another 6.5 per cent in the week ended July 11 and by 5.4 per cent in the week that ended on July 18.

Consumer sentiments in urban India were a lot less sure-footed.

They fell by 4.2 per cent in the week ended July 4 but rose by 6.1 per cent in the week ended July 11 and then remained flat in the week ended July 18.

As a result, they ended the first three weeks of July with a modest 1.7 per cent increase.

Perhaps, the rural-urban divergence in consumer sentiments reflects the movements in employment in the two regions.

The employment rate improved by 6.7 per cent in the first three weeks of July in rural India.

Urban India on the other hand, saw a much smaller improvement of 1.5 per cent in the employment rate.

Sentiments in rural India have improved essentially because less people feel that their economic conditions have worsened over the past one year and also because less people are pessimistic about the future.

But there isn't much improvement in the people who feel that their own conditions have improved.

There is less despondency in rural households on the state of economic well-being but there isn't any improvement in the spread of growth.

Households reporting growth continue to remain abysmally low.

In the week ended July 18, only 4.6 per cent of the rural household respondents said that their incomes were higher than a year ago.

This is worse than 5.4 per cent who said that their incomes were better than a year ago in the week ended June 27.

Similarly, the proportion of rural households that said this is a better time to buy consumer durables dropped from 2.3 per cent as of the week ended June 27 to 1.9 per cent in the week ended July 18.

Although rural households do not yet reflect optimism on their current economic conditions they have started showing greater confidence in the future.

Like in the earlier case, we make comparisons between the week ended June 27 and the week ended July 18.

The proportion of rural households that expect their incomes to improve in a year has gone up from 2.5 per cent to 3.2 per cent.

This is abysmally low, but the consolation in the numbers is that they are moving in the right direction.

The proportion of rural households that expect the financial and business environment to improve in the coming twelve months has increased from 2.8 per cent to 4.7 per cent.

And the proportion of households that expect financial and business conditions to improve in the coming five years has increased from 2.8 per cent to 4.5 per cent.

The improvement in rural consumer sentiments could be the result of a revival in the monsoon.

In the weeks ended June 30 and July 7, the monsoon precipitation was 30 per cent and 46 per cent below normal. In the week ended July 14, the precipitation was only 7 per cent below normal.

The monsoon this year seems fickle. Early indications suggest that the week ended July 21 may not be great.

Errant monsoons have had an impact on kharif sowing. As of July 16, these were down 11.6 per cent compared to a year ago.

All major crops except for sugarcane, arhar, sunflower seeds and jute had recorded lower sowing compared to a year ago.

Prices have been high and the IMD continues to talk of a monsoon revival and normal monsoons this year.

Hopes therefore are alive of a reasonable if not robust turnaround.

Much of the corporate sector reposes faith in rural India to fuel its growth.

Post the two COVID-19 shocks, NBFCs have been complaining of increased delinquencies. It will help these companies that the proportion of households reporting a fall in income has started to fall.

Of course, it is important this is just the beginning.

Fast moving consumer goods companies have mostly held the view that the urban markets have saturated for them and further growth is possible mostly in rural India.

But, for these markets to grow it is imperative that there is an increase in households that report an increase in income.

A mere fall in households reporting a fall is not enough.

Consumer goods companies need to see an increase in households reporting willingness to buy. This is still some distance into the future.

© 2025

© 2025