Photographs: Dominic Xavier/Rediff.com Priyadarshini Dembla

Buying a wrong insurance policy can give you nightmares when it comes to settling claims. Then there are other issues like cost, riders etc. Here's a seven-point checklist to help you buy an insurance policy that YOU need.

If you have dependents, then life insurance should form an integral part of your financial planning. However, choosing the appropriate policy with the right coverage is important to ensure that the very purpose of insurance is met.

Here is a step-by-step guide on getting insured the right way.

1. Calculate the amount of insurance you need

Even those who realise the need for life insurance struggle to gauge the exact amount required. This is a very crucial factor because if you mis-calculate, you could end up putting your family in a very tight spot.

The exact amount will depend on how many dependents you have, if your spouse is also earning, whether your children are still young and have education expenses or are employed, your liabilities and assets, and other sources of income.

You will also have to take into account your lifestyle and future financial requirements, such as a marriage in the family.

Please click NEXT to continue reading

Courtesy ![]()

2. Look at the cost factor

Photographs: Dominic Xavier/Rediff.com

Go through all the charges applicable -- premium charges, administration fees, mortality charges, fund management charge and rider charges, if any.

The insurance regulator, the Insurance Regulatory and Development Authority, or IRDA, recently announced a number of changes with regards to these charges to make insurance policies more investor friendly.

Check how much it would cost you to buy a policy online rather than via an agent.

Also compare similar products available in the market and the cost associated to know whether one insurer is being unreasonably higher. At the same time, don’t just rush to an insurance company just because the policy is much cheaper.

Please click NEXT to continue reading

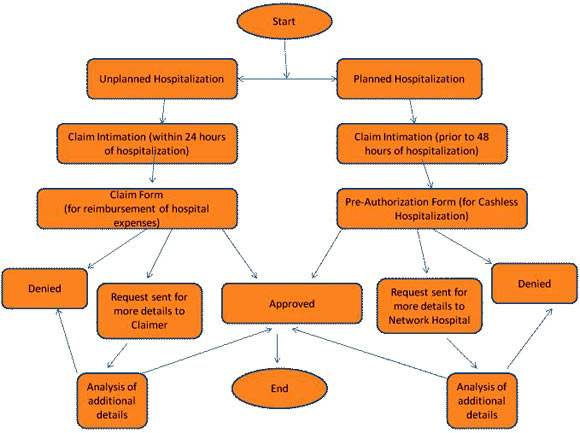

3. Know your insurer

Photographs: Rediff Archives

We buy insurance to secure us and our family against any unforeseen event. But have you ever considered the situation where your family is not able to obtain the money you were insured for due to some reason or the other?

One way to protect yourself against such an eventuality is to do some amount of legwork before you sign up with a company.

Ask your friends, relatives and colleagues about their experiences with various insurance companies. Check out the claim settlement ratio which is the percentage of claims settled by an insurance company against the number of claims submitted.

If 100 people submit claims and 80 are paid up, the claim settlement ratio is 80 per cent. The higher the ratio, the better.

According to IRDA, six life insurance companies had a claim settlement ratio of above 90 per cent in FY2012-13. Those were LIC (97.7 per cent), ICICI Prudential Life, HDFC Life, SBI Life, Max Life and Kotak Life (92 per cent).

Don't be lured by fancy offerings, swayed by your insurance agent, or taken up with low premium products. Do the necessary ground work.

Please click NEXT to continue reading

4. Check the riders on offer

Photographs: Dominic Xavier/Rediff.com

Look at the riders on offer and what they will cost. Or, if none are available see if your request for one is admissible.

Many insurance companies provide riders such as an accidental death rider which would double the value of your life insurance policy.

Similarly, be on top of the disclaimers attached to your policy. Going through the policy document could indeed seem like a task but spending a little time trying to understand it could help you in the long run avoid any conflict with the insurance company at the time of claim.

Review the amount covered, the term of cover, the deductible charges, and so on and so forth. Read the agreement carefully to know of the exclusions which the policy may not cover.

Please click NEXT to continue reading

5. Don't go overboard buying policies

Photographs: Dominic Xavier/Rediff.com

Buying too many life insurance policies does no good. This is often the case when individuals blindly purchase policies to meet the limit under Section 80C.

Insurance is sold via agents who earn commissions from life insurance companies. Don't blindly go for what your agent recommends since s/he may be looking at policies which earn high commissions.

Please click NEXT to continue reading

6. Don't be afraid to ask for help

Photographs: Uttam Ghosh/Rediff.com

You may not have the time, inclination or the objectivity to get an insurance plan in place. You could take the help of a certified financial advisor who can guide you through the entire process and help you make a sound decision.

Please click NEXT to continue reading

7. Revisit your insurance needs

Photographs: Rediff Archives

There could be a change in your situation. For instance, you might have taken a life insurance policy when you were married. But now that you have a child, it's time to take a fresh look at the amount you are insured for.

Also, be aware of what you have bought and the tenure of the policy. If your policy has a 10-year time frame, be sure to relook your life insurance requirements before it lapses.

Comment

article