Taxpayers can claim a deduction on tuition fees for a maximum of two children.

This time of the year, the salaried get busy finalising their tax-saving investments and other deductions, after employers send the investment declaration form.

If you fail to give the details, with proofs, the organisation would start deducting the applicable taxes from your salary, resulting in huge cuts over the next four months.

While you can claim a refund later when filing returns, it's better to get the correct salary now.

Also, all the proofs will go to the tax department through the employer rather than you maintaining these, in case the assessing officer calls for scrutiny.

The first step is to calculate the money you will earn in the next four months, deduct the expenses and arrive at the amount you can spare each month for saving tax.

Accordingly, plan the monthly outgo for each instrument and product.

For instance, if you want to invest in an equity-linked savings scheme (ELSS) and public provident fund (PPF) and have Rs 20,000 of surplus each month, you can accordingly allocate the proportion of money for each of them.

Investments

When saving for tax, the best instruments are those in the exempt-exempt-exempt (EEE) tax regime.

When saving for tax, the best instruments are those in the exempt-exempt-exempt (EEE) tax regime.

These get a deduction on investment, and there's no tax on accrual or withdrawal. These include PPF and ELSS.

If you are in the lowest income tax bracket of 10 per cent, the annually tax liability will be Rs 23,695 or lower, depending on your income.

This is about Rs 1,975 each month. Experts say those in the lowest tax bracket should split their investment between PPF and ELSS.

A majority of the money can go to PPF, say 60-70 per cent. This is because PPF has a longer lock-in, of 15 years, whereas many break their ELSS investments when creating assets such as buying a house.

At an annual interest rate of 8.7 per cent, PPF is one of the best options for retirement planning.

Those in the 20 per cent tax bracket will have an annual tax liability of Rs 1.29 lakh or less, depending on your income, which is Rs 10,729 a month.

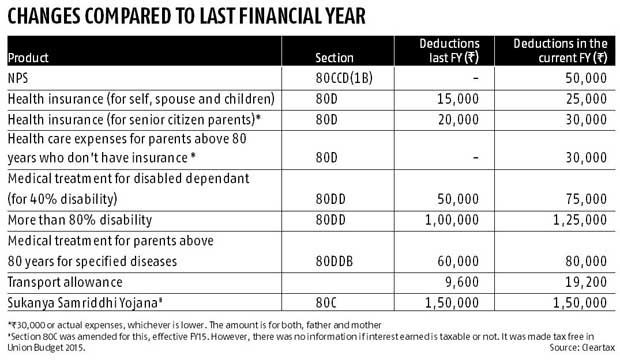

Experts say these individuals should look at the National Pension System (NPS), if they have exhausted the Section 80C limit.

There's an additional deduction of Rs 50,000, under Section 80CCD (1B), for contributions to NPS.

For those in the 30 per cent tax bracket, the employee provident fund (EPF) takes care of the majority of the portion of Section 80C deductions.

Many of these individuals also have a housing loan and this will help to exhaust the remaining portion of the Rs 1.5 lakh deductions available under Section 80C.

However, financial planners say individuals in this tax bracket should also continue to invest in PPF.

If they have an investment portfolio, the PPF investments can be part of the debt portion. These individuals should also make use of the NPS investments that will form part of their retirement corpus.

Those who have bought a house also get a deduction on the interest portion of the home loan under Section 24.

If they are staying in it, this is restricted to Rs 2 lakh. If the flat is let out, the entire interest portion can be claimed as deduction.

Other deductions

Other deductions

This year, Finance Minister Arun Jaitley has increased the limit of deduction a person can get for health insurance under Section 80D.

Now, one can claim a Rs 25,000 deduction, compared with Rs 15,000 earlier for health insurance that covers self, spouse and children.

Also, if your parents are senior citizens and you pay for their mediclaim, you can get a deduction of Rs 30,000, against Rs 20,000 earlier.

Taxpayers can also claim a deduction on tuition fees for a maximum of two children.

Husband and wife can separately claim the deductions and, therefore, the maximum deduction a couple can claim here is for four children.

This can be claimed for tuition fee paid for full-time courses at a recognised institution within India.

Less-known deductions

Archit Gupta, founder and chief executive of ClearTax, an I-T return filing website, says those who earn less than Rs 5 lakh annually can claim a maximum deduction of Rs 2,000 under Section 87A.

In the case of parents over 80 years, who might not be eligible for insurance, medical expenses up to Rs 30,000 can be claimed. The maximum deduction which can be claimed for both parents is limited to Rs 30,000.

Gupta also notes that taxpayers can claim additional deductions for parents over 80 years for medical treatment if they are suffering from specified diseases (such as cancer and neurological diseases).

In the current Budget, it's been raised from Rs 60,000 to Rs 80,000.

Instruments to avoid

Experts say those doing tax planning at the last moment usually end up putting money in unit-linked insurance plans (Ulips) or traditional insurance policies.

These are instruments they should avoid. Steven Fernandes, a certified financial planner, says rather than investing in the Sukanya Samridhi Scheme, a person can look at ELSS for the same purpose, as the latter can earn better returns over the long term.

Malhar Majumder, a certified financial planner, says one should avoid using a credit card to pay for instruments such mediclaim that would help in tax deduction.

If the person does not pay back on time, the interest charged will be much higher than the tax saved.

© 2025

© 2025